Real Data: Preliminary Analyais

Author: Spark Tseung

Last Modified: Sept 15, 2020

Introduction

In this document, we will perform some preliminary analysis and data

cleaning of the French Motor Third-Party Liability dataset

(freMTPLfreq and freMTPLsev in the CASdatasets package). The

dataset can be loaded using the following code.

library(CASdatasets)

data(freMTPLfreq, freMTPLsev)

Data Cleaning

The freMTPLfreq contains a number of policy features (covariates) and

the number of claims filed by each policy.

head(freMTPLfreq)

## PolicyID ClaimNb Exposure Power CarAge DriverAge

## 1 1 0 0.09 g 0 46

## 2 2 0 0.84 g 0 46

## 3 3 0 0.52 f 2 38

## 4 4 0 0.45 f 2 38

## 5 5 0 0.15 g 0 41

## 6 6 0 0.75 g 0 41

## Brand Gas Region Density

## 1 Japanese (except Nissan) or Korean Diesel Aquitaine 76

## 2 Japanese (except Nissan) or Korean Diesel Aquitaine 76

## 3 Japanese (except Nissan) or Korean Regular Nord-Pas-de-Calais 3003

## 4 Japanese (except Nissan) or Korean Regular Nord-Pas-de-Calais 3003

## 5 Japanese (except Nissan) or Korean Diesel Pays-de-la-Loire 60

## 6 Japanese (except Nissan) or Korean Diesel Pays-de-la-Loire 60

summary(freMTPLfreq)

## PolicyID ClaimNb Exposure Power

## 1 : 1 Min. :0.00000 Min. :0.002732 f :95718

## 2 : 1 1st Qu.:0.00000 1st Qu.:0.200000 g :91198

## 3 : 1 Median :0.00000 Median :0.540000 e :77022

## 4 : 1 Mean :0.03916 Mean :0.561088 d :68014

## 5 : 1 3rd Qu.:0.00000 3rd Qu.:1.000000 h :26698

## 6 : 1 Max. :4.00000 Max. :1.990000 j :18038

## (Other):413163 (Other):36481

## CarAge DriverAge Brand

## Min. : 0.000 Min. :18.00 Fiat : 16723

## 1st Qu.: 3.000 1st Qu.:34.00 Japanese (except Nissan) or Korean: 79060

## Median : 7.000 Median :44.00 Mercedes, Chrysler or BMW : 19280

## Mean : 7.532 Mean :45.32 Opel, General Motors or Ford : 37402

## 3rd Qu.: 12.000 3rd Qu.:54.00 other : 9866

## Max. :100.000 Max. :99.00 Renault, Nissan or Citroen :218200

## Volkswagen, Audi, Skoda or Seat : 32638

## Gas Region Density

## Diesel :205945 Centre :160601 Min. : 2

## Regular:207224 Ile-de-France : 69791 1st Qu.: 67

## Bretagne : 42122 Median : 287

## Pays-de-la-Loire : 38751 Mean : 1985

## Aquitaine : 31329 3rd Qu.: 1410

## Nord-Pas-de-Calais: 27285 Max. :27000

## (Other) : 43290

Claim Number

The response ClaimNb is significantly zero-inflated, and very few

policyholders have more than one claim.

summary(freMTPLfreq$ClaimNb)

## Min. 1st Qu. Median Mean 3rd Qu. Max.

## 0.00000 0.00000 0.00000 0.03916 0.00000 4.00000

table(freMTPLfreq$ClaimNb)

##

## 0 1 2 3 4

## 397779 14633 726 28 3

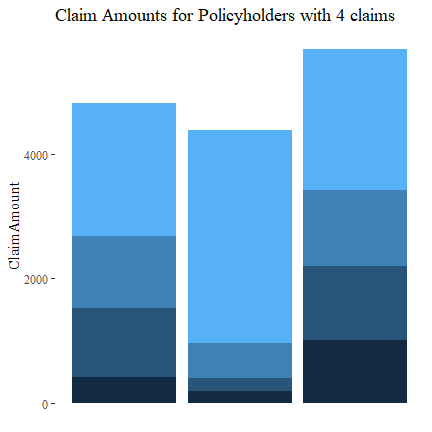

Let’s see which policyholders have 4 claims and their claim amounts. There doesn’t seem to be any discernible pattern.

# Which policies have 4 claims?

four.idx = which(freMTPLfreq$ClaimNb==4)

# freMTPLfreq[four.idx,]

# What are the claim amounts?

four.id = freMTPLfreq[four.idx,1]

df4 = freMTPLsev[freMTPLsev[,1] %in% four.id,]

df4

## PolicyID ClaimAmount

## 322 311457 1011

## 323 311457 1221

## 329 311457 2267

## 330 311457 1189

## 1713 226856 196

## 1714 226856 3411

## 1715 226856 201

## 1716 226856 570

## 13086 18652 417

## 13118 18652 1155

## 13124 18652 2129

## 13254 18652 1110

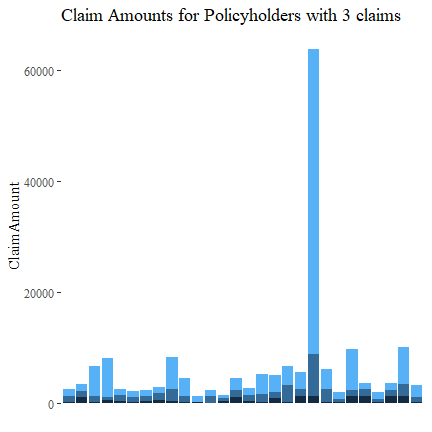

Similarly, let’s look at policyholders with 3 claims. There is no discernible pattern.

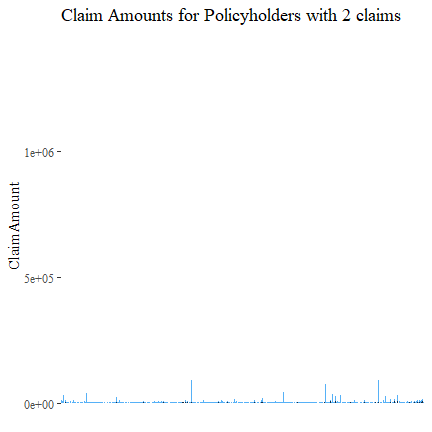

Now those with 2 claims.

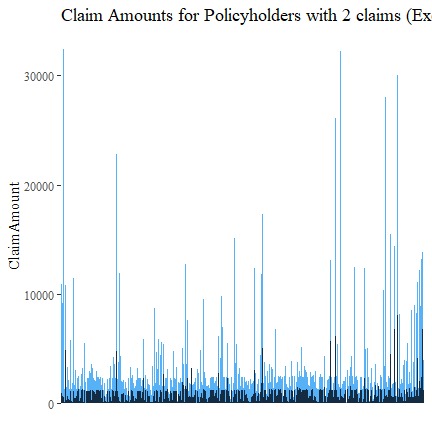

There are some policyholder with extremely large claims. Let’s remove the highest 10 and then plot again. There is no discernible pattern.

We will not separately plot policyholders with only one claim (see also the next subsection on Claim Amount).

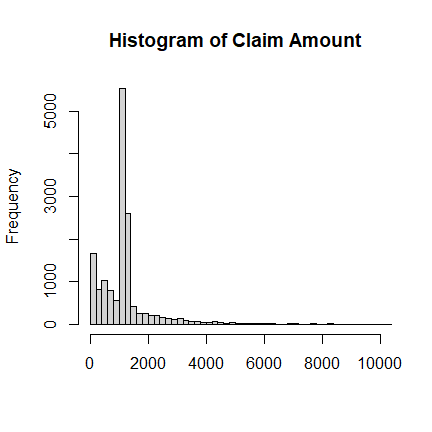

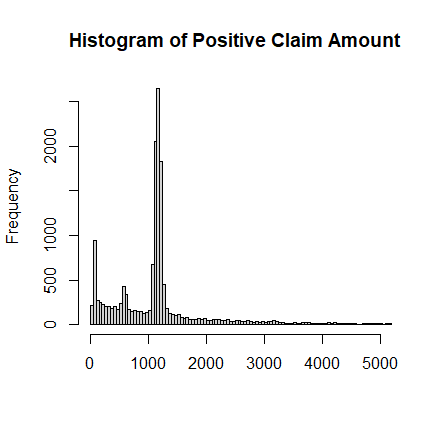

Claim Amount

The freMTPLsev contains the PolicyID and ClaimAmount for those who

have filed claims. Some summary statistics and a histogram are shown

below. It is multi-modal, over-dispersed, right-skewed and heavy-tailed.

# Summary Staitistics

summary(freMTPLsev$ClaimAmount)

## Min. 1st Qu. Median Mean 3rd Qu. Max.

## 2 698 1156 2130 1243 2036833

mean(freMTPLsev$ClaimAmount)

## [1] 2129.972

sd(freMTPLsev$ClaimAmount)

## [1] 21063.64

skewness(freMTPLsev$ClaimAmount)

## [1] 75.13135

kurtosis(freMTPLsev$ClaimAmount)

## [1] 6601.197

Clearly, there are some very large outliers of ClaimAmount. We will

ignore some of these data points.

# Some Quantiles

quantile(freMTPLsev$ClaimAmount, c(0.90, 0.95, 0.99, 0.995, 0.9975, 0.999, 0.9999))

## 90% 95% 99% 99.5% 99.75% 99.9% 99.99%

## 2583.00 4284.00 16109.40 35431.50 68302.65 131834.02 725143.52

# Beyond 2 SD away from mean

mean(freMTPLsev$ClaimAmount) + 2*sd(freMTPLsev$ClaimAmount)

## [1] 44257.26

# Extremely large claims

freMTPLsev$ClaimAmount[freMTPLsev$ClaimAmount>70000]

## [1] 73417 85294 125705 86331 114936 96906 85804 72479 116379

## [10] 301302 137003 72960 132502 254944 120931 152135 2036833 306559

## [19] 128791 115412 92031 205090 240884 1402330 186612 281403 71253

## [28] 182568 86466 115511 209462 182467 181697 75060 89598 210837

# We will delete claim amounts > 100000

sev.cutoff = 100000

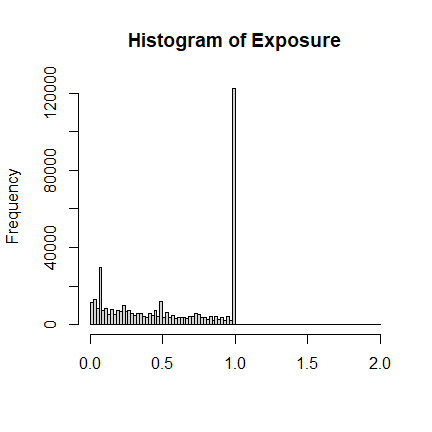

Exposure

The variable Exposure in freMTPLfreq contains the exposure (i.e. how

long the policy covers). Most are one-year or less, with a few policies

longer than that but less than two years.

# Summary Staitistics

summary(freMTPLfreq$Exposure)

## Min. 1st Qu. Median Mean 3rd Qu. Max.

## 0.002732 0.200000 0.540000 0.561088 1.000000 1.990000

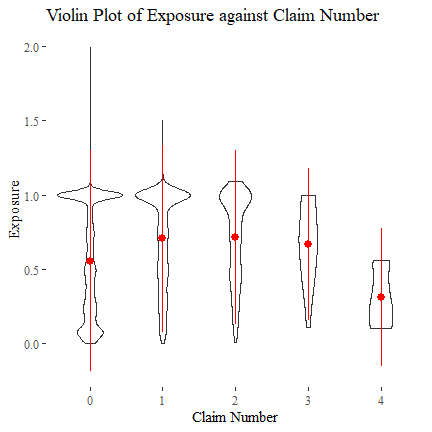

One may expect that, the longer the policy exposure, the more likely that a claim will be made (all others held constant). However, the following plot does not support this, as those with 3 or 4 claims can also have a quite short exposure. Meanwhile, a number of policies with zero claim tend to have shorter exposures.

We will also exclude policies with Exposure > 1 from our analysis.

exposure.cutoff = 1

# Exposure deleted

freMTPLfreq$Exposure[freMTPLfreq$Exposure>exposure.cutoff]

## [1] 1.99 1.50 1.53 1.48 1.09 1.01 1.01 1.34 1.46 1.34 1.07 1.04 1.08 1.01 1.07

## [16] 1.01 1.06 1.02 1.08 1.01 1.12 1.15 1.13 1.05 1.01 1.08 1.01 1.07 1.15 1.02

## [31] 1.01 1.01 1.03 1.16 1.02 1.08 1.03 1.02 1.15 1.03 1.01 1.01 1.02 1.01 1.02

## [46] 1.02 1.01 1.22 1.04 1.01 1.03 1.01 1.01 1.04 1.13 1.02 1.01 1.04 1.23 1.01

## [61] 1.01 1.16 1.01 1.01 1.02 1.01 1.01 1.02 1.09 1.04 1.04 1.01 1.01 1.41 1.03

## [76] 1.03 1.01 1.02 1.01 1.02 1.03 1.05 1.01 1.02 1.01 1.11 1.01 1.01 1.02 1.01

## [91] 1.23 1.05 1.01 1.09 1.01 1.02 1.11 1.09 1.23 1.02 1.01 1.34 1.38 1.08 1.14

## [106] 1.23 1.01 1.25 1.02 1.07 1.05 1.03 1.09 1.43 1.04 1.02 1.02 1.02 1.02 1.01

## [121] 1.01 1.02 1.25 1.02 1.09 1.12 1.08 1.01 1.01 1.04 1.01 1.01 1.14 1.03 1.23

## [136] 1.41 1.09 1.01 1.07 1.03 1.01 1.01 1.02 1.05 1.06 1.03 1.06 1.07 1.03 1.03

## [151] 1.02 1.01 1.11 1.01 1.01 1.01 1.03 1.20 1.01 1.06 1.03 1.10 1.26 1.02 1.01

## [166] 1.04 1.01 1.03 1.01 1.02 1.21 1.04 1.03 1.01 1.01 1.04 1.02 1.03 1.03 1.05

## [181] 1.03 1.10 1.01 1.02 1.15 1.01 1.01 1.01 1.03 1.07 1.18 1.02 1.01 1.02 1.24

## [196] 1.03 1.36 1.03 1.02 1.03 1.06 1.02 1.01 1.20 1.48 1.01 1.01 1.01 1.03 1.04

## [211] 1.10 1.36 1.02 1.01 1.01 1.01 1.01 1.06 1.13 1.01 1.07 1.02 1.01 1.18 1.07

## [226] 1.04 1.03 1.34 1.01 1.43 1.13 1.02 1.03 1.65 1.03 1.02 1.13 1.98 1.04 1.11

## [241] 1.03 1.07 1.19 1.17 1.24 1.06 1.12 1.18 1.12 1.02 1.01 1.08 1.18 1.07 1.27

## [256] 1.25 1.11 1.03 1.11 1.06 1.18 1.04 1.01 1.07 1.56 1.06 1.01 1.03 1.03 1.17

## [271] 1.06 1.24 1.19 1.03 1.23 1.10 1.03 1.03 1.08 1.17 1.03 1.11 1.12 1.04 1.07

## [286] 1.03 1.05 1.05 1.02 1.05 1.01 1.28 1.01 1.01 1.09 1.32 1.22 1.43 1.17 1.12

## [301] 1.33 1.01 1.30 1.52 1.35 1.22 1.03 1.12 1.05 1.04 1.01 1.35 1.16 1.01 1.05

## [316] 1.01 1.30 1.90 1.41 1.46 1.50 1.12 1.19 1.05 1.03 1.75 1.39 1.27 1.90 1.70

## [331] 1.27 1.49 1.64 1.48 1.48 1.07 1.07 1.01 1.14 1.07 1.24 1.15 1.11 1.03 1.01

## [346] 1.02 1.01 1.01 1.03 1.04 1.15 1.15 1.02 1.01 1.23 1.18 1.15 1.10 1.06 1.07

## [361] 1.13 1.09 1.06 1.06 1.03 1.04 1.19 1.05 1.11 1.10 1.01 1.01 1.14 1.18 1.03

## [376] 1.02 1.03 1.19 1.10 1.01 1.03 1.16 1.03 1.02 1.01 1.01 1.02 1.07 1.02 1.04

## [391] 1.01 1.03 1.01 1.02 1.01 1.01 1.01 1.01 1.07 1.08 1.06 1.16 1.03 1.01 1.02

## [406] 1.03 1.03 1.03 1.04 1.03 1.03 1.01 1.04 1.01 1.13 1.11 1.08 1.09 1.01 1.18

## [421] 1.01

# Data to ignore due to Exposure > 1: 421 entries.

didx.exposure = (freMTPLfreq$Exposure>1)

summary(didx.exposure)

## Mode FALSE TRUE

## logical 412748 421

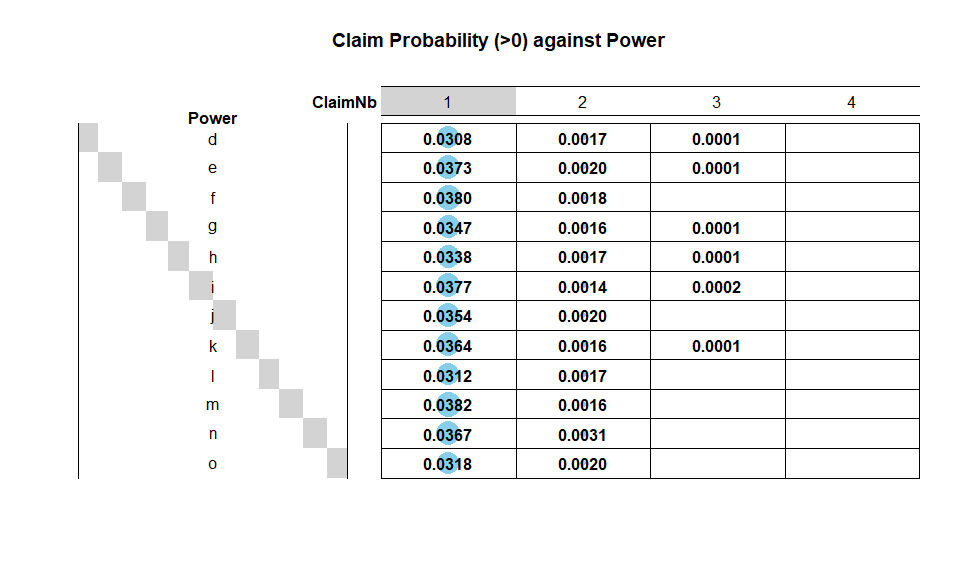

Power

Power is a categorical variable describing the power of a car. There

is not any data issue. The majority of policies have car power of type

d to j. A simple chi-squared test on contingency table also suggests

that Power and ClaimNb are not independent: power types e,

f, m and n tend to have more claims.

summary(freMTPLfreq$Power)

## d e f g h i j k l m n o

## 68014 77022 95718 91198 26698 17616 18038 9537 4681 1832 1307 1508

PNbtable = table(freMTPLfreq$Power, freMTPLfreq$ClaimNb)

PNbtable

##

## 0 1 2 3 4

## d 65791 2098 116 7 2

## e 73988 2875 152 6 1

## f 91905 3633 176 4 0

## g 87887 3163 143 5 0

## h 25748 902 46 2 0

## i 16924 665 24 3 0

## j 17364 638 36 0 0

## k 9174 347 15 1 0

## l 4527 146 8 0 0

## m 1759 70 3 0 0

## n 1255 48 4 0 0

## o 1457 48 3 0 0

chisq = chisq.test(PNbtable)

chisq

##

## Pearson's Chi-squared test

##

## data: PNbtable

## X-squared = 100.35, df = 44, p-value = 2.737e-06

# Probability of making a claim

1-t(round(sweep(PNbtable, 1, rowSums(PNbtable), FUN = "/"),4)[,1])

## d e f g h i j k l m

## [1,] 0.0327 0.0394 0.0398 0.0363 0.0356 0.0393 0.0374 0.0381 0.0329 0.0398

## n o

## [1,] 0.0398 0.0338

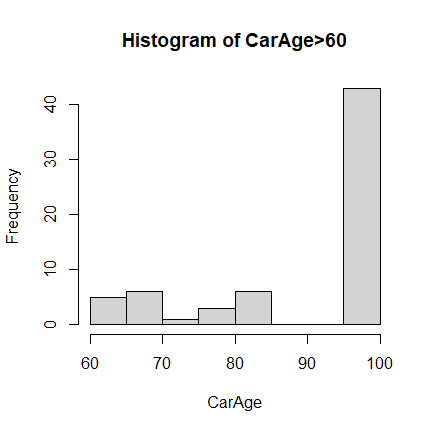

Car Age

For CarAge, the extremely large values seem quite suspicious.

# Check the large values in CarAge

freMTPLfreq$CarAge[freMTPLfreq$CarAge>90]

## [1] 100 100 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99

## [20] 99 99 99 99 100 100 100 100 100 100 100 100 100 100 100 100 100 100 100

## [39] 100 100 100 100 100

Based on the data summary and histogram plot, it is reasonable to assume

(without further information available) that 99 and 100 are used for

either missing or error data entries. There are also some extremely old

cars. We will ignore all these data points when conducting further

analysis.

# Some Quantiles

quantile(freMTPLfreq$CarAge, c(0.90, 0.95, 0.99, 0.995, 0.9975, 0.999, 0.9999))

## 90% 95% 99% 99.5% 99.75% 99.9% 99.99%

## 15 17 22 25 29 34 99

# Beyond 2 SD away from mean

mean(freMTPLfreq$CarAge) + 2*sd(freMTPLfreq$CarAge)

## [1] 19.05843

# We will delete CarAge > 30

carage.cutoff = 30

# Data to ignore due to invalid CarAge: 846 entries.

didx.carage = (freMTPLfreq$CarAge>carage.cutoff)

summary(didx.carage)

## Mode FALSE TRUE

## logical 412323 846

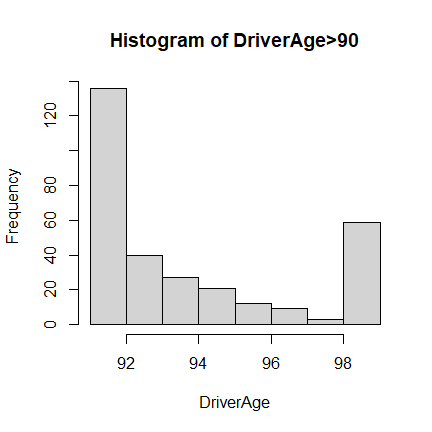

Driver Age

For DriverAge, we take a similar approach as in CarAge.

# Large values

freMTPLfreq$DriverAge[freMTPLfreq$DriverAge>90]

## [1] 95 93 91 99 91 99 99 95 91 99 95 99 99 99 99 99 99 99 99 99 99 99 99 99 99

## [26] 99 99 99 99 99 99 99 99 99 99 91 94 99 99 95 93 93 99 99 99 99 93 93 99 99

## [51] 99 99 99 99 99 92 92 91 91 93 92 91 99 92 99 99 99 99 99 91 99 92 99 99 99

## [76] 99 93 94 94 95 99 99 99 99 99 95 99 96 91 91 91 91 91 91 91 92 92 96 91 92

## [101] 95 95 94 91 91 94 94 94 92 93 93 93 92 91 91 91 91 92 91 91 91 91 91 94 95

## [126] 95 96 96 97 92 92 92 92 92 92 91 91 93 91 97 92 93 96 92 91 95 95 91 91 95

## [151] 95 92 93 93 94 91 94 91 91 94 94 91 91 91 92 91 92 91 92 93 92 91 92 91 96

## [176] 97 97 91 98 93 93 93 93 91 93 91 91 92 94 91 93 94 97 91 91 93 92 96 92 96

## [201] 96 96 91 93 93 94 93 93 94 95 92 95 91 92 92 92 92 92 93 92 93 94 93 92 92

## [226] 97 92 91 99 94 94 91 94 92 94 91 92 91 91 91 92 93 91 91 91 95 91 92 94 91

## [251] 98 92 92 91 92 91 94 93 97 93 97 97 91 91 92 91 91 91 91 91 91 91 95 91 91

## [276] 91 91 91 94 94 95 95 91 96 93 96 91 92 93 93 93 91 91 91 91 91 93 94 94 95

## [301] 91 91 93 93 98 91 93

Based on the data summary and histogram plot, it is reasonable to assume

(without further information available) that 99 is used for either

missing or error data entries, or just any age larger than or equal to

99. We will also ignore these data points when conducting further

analysis.

# Data to ignore due to ambiguous DriverAge: 59 entries.

didx.driverage = (freMTPLfreq$DriverAge==99)

summary(didx.driverage)

## Mode FALSE TRUE

## logical 413110 59

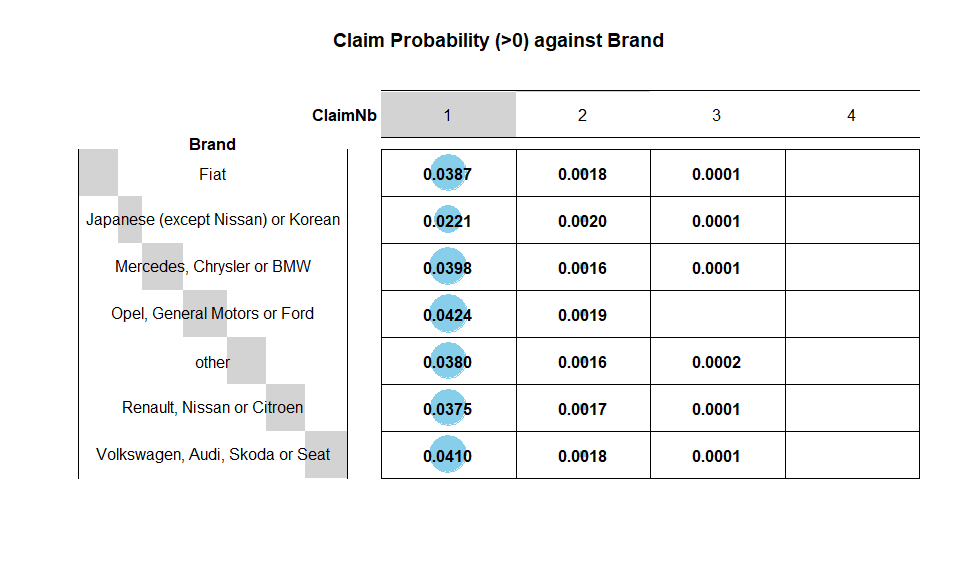

Brand

Brand is also a categorical variable, and there is no invalid data

point. The analysis is similar to Power. Brand is also not

independent of ClaimNb: It appears that General Motors or Ford,

Volkswagen, Audi, Skoda or Seat and Mercedes, Chrysler or BMW Opel

are riskier than other brands.

summary(freMTPLfreq$Brand)

## Fiat Japanese (except Nissan) or Korean

## 16723 79060

## Mercedes, Chrysler or BMW Opel, General Motors or Ford

## 19280 37402

## other Renault, Nissan or Citroen

## 9866 218200

## Volkswagen, Audi, Skoda or Seat

## 32638

BNbtable = table(freMTPLfreq$Brand, freMTPLfreq$ClaimNb)

BNbtable

##

## 0 1 2 3 4

## Fiat 16043 648 30 2 0

## Japanese (except Nissan) or Korean 77150 1748 157 4 1

## Mercedes, Chrysler or BMW 18481 767 30 2 0

## Opel, General Motors or Ford 35746 1584 70 1 1

## other 9473 375 16 2 0

## Renault, Nissan or Citroen 209649 8173 365 13 0

## Volkswagen, Audi, Skoda or Seat 31237 1338 58 4 1

chisq = chisq.test(BNbtable)

chisq

##

## Pearson's Chi-squared test

##

## data: BNbtable

## X-squared = 553.76, df = 24, p-value < 2.2e-16

# Probability of making a claim

1-t(round(sweep(BNbtable, 1, rowSums(BNbtable), FUN = "/"),4)[,1])

## Fiat Japanese (except Nissan) or Korean Mercedes, Chrysler or BMW

## [1,] 0.0407 0.0242 0.0414

## Opel, General Motors or Ford other Renault, Nissan or Citroen

## [1,] 0.0443 0.0398 0.0392

## Volkswagen, Audi, Skoda or Seat

## [1,] 0.0429

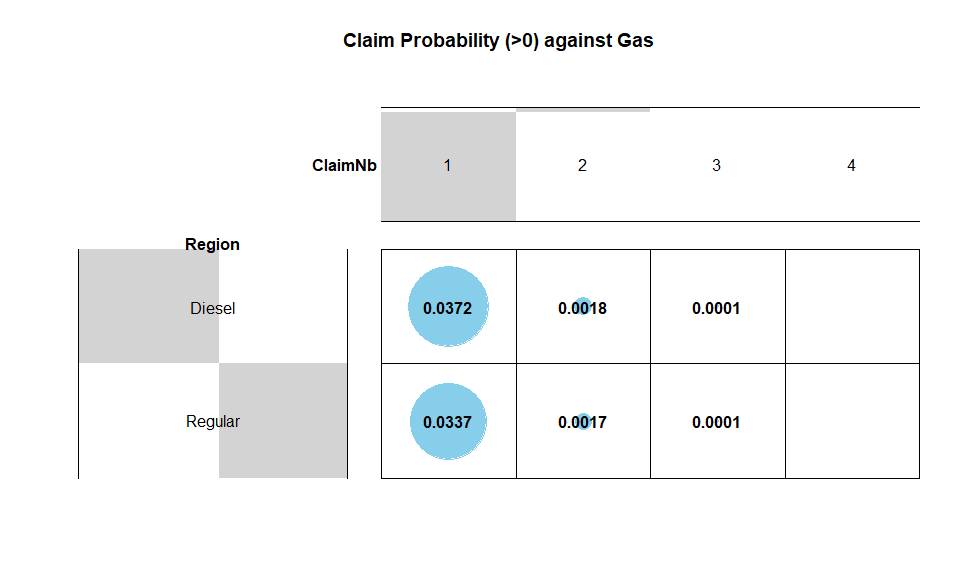

Gas

Gas is a categorical with only two levels: Regular and Diesel. All

data entries are valid. There are roughly the same number of cars for

each gas type, but Diesel cars tend to have a higher probability of

claims.

summary(freMTPLfreq$Gas)

## Diesel Regular

## 205945 207224

GNbtable = table(freMTPLfreq$Gas, freMTPLfreq$ClaimNb)

GNbtable

##

## 0 1 2 3 4

## Diesel 197904 7655 369 15 2

## Regular 199875 6978 357 13 1

chisq = chisq.test(GNbtable)

chisq

##

## Pearson's Chi-squared test

##

## data: GNbtable

## X-squared = 37.804, df = 4, p-value = 1.23e-07

# Probability of making a claim

1-t(round(sweep(GNbtable, 1, rowSums(GNbtable), FUN = "/"),4)[,1])

## Diesel Regular

## [1,] 0.039 0.0355

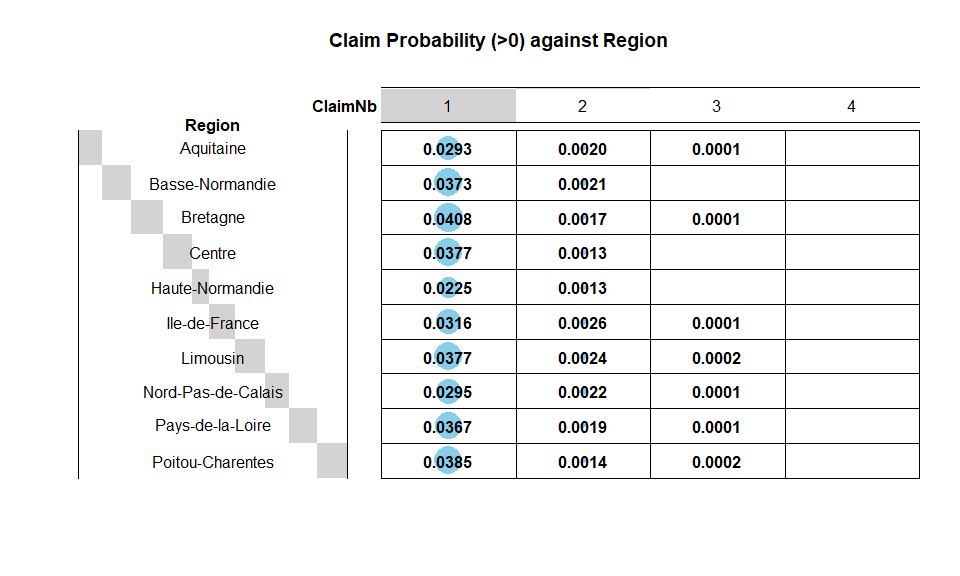

Region

There are a number of regions where the policies are issued. All data

entries are valid. Regions with a higher probability of claims are

Bretagne,Limousin and Poitou-Charentes.

summary(freMTPLfreq$Region)

## Aquitaine Basse-Normandie Bretagne Centre

## 31329 10893 42122 160601

## Haute-Normandie Ile-de-France Limousin Nord-Pas-de-Calais

## 8784 69791 4567 27285

## Pays-de-la-Loire Poitou-Charentes

## 38751 19046

RNbtable = table(freMTPLfreq$Region, freMTPLfreq$ClaimNb)

RNbtable

##

## 0 1 2 3 4

## Aquitaine 30344 919 62 4 0

## Basse-Normandie 10464 406 23 0 0

## Bretagne 40329 1718 72 3 0

## Centre 154339 6053 206 2 1

## Haute-Normandie 8575 198 11 0 0

## Ile-de-France 67398 2205 179 8 1

## Limousin 4383 172 11 1 0

## Nord-Pas-de-Calais 26413 806 61 4 1

## Pays-de-la-Loire 37253 1422 74 2 0

## Poitou-Charentes 18281 734 27 4 0

chisq = chisq.test(RNbtable)

chisq

##

## Pearson's Chi-squared test

##

## data: RNbtable

## X-squared = 285.13, df = 36, p-value < 2.2e-16

# Probability of making a claim

1-t(round(sweep(RNbtable, 1, rowSums(RNbtable), FUN = "/"),4)[,1])

## Aquitaine Basse-Normandie Bretagne Centre Haute-Normandie Ile-de-France

## [1,] 0.0314 0.0394 0.0426 0.039 0.0238 0.0343

## Limousin Nord-Pas-de-Calais Pays-de-la-Loire Poitou-Charentes

## [1,] 0.0403 0.032 0.0387 0.0402

Density

The variable Density for population density is continuous. There is no

invalid data point. Also, it seems that Density has a finer resolution

than Region.

# Summary Staitistics

summary(freMTPLfreq$Density)

## Min. 1st Qu. Median Mean 3rd Qu. Max.

## 2 67 287 1985 1410 27000

One may expect that, the higher the population density, the more likely that a claim will be made (all others held constant). This is somewhat illustrated by the following violin plot.

Based on the previous analysis, we only need to delete invalid data or

outliers based on Exposure, CarAge and DriverAge. In total, there

are 1324 data points deleted. Data cleaning based for ClaimAmount is

deferred to the next section.

Preliminary Analysis of Claim Amount

Our primary interest is the response variable ClaimAmount. We first

merge the dataframes freMTPLfreq and freMTPLsev, and then analyze

the relationship between ClaimAmount and the policy covariates.

# Merge two dataframes

df = merge(x = freMTPLfreq, y = freMTPLsev, all = TRUE)

# Zero claim amount is matched to NA: replace them by zero

df$ClaimAmount[is.na(df$ClaimAmount)] = 0

summary(df)

## PolicyID ClaimNb Exposure Power

## 18652 : 4 Min. :0.00000 Min. :0.002732 f :95902

## 226856 : 4 1st Qu.:0.00000 1st Qu.:0.200000 g :91351

## 311457 : 4 Median :0.00000 Median :0.540000 e :77189

## 15608 : 3 Mean :0.04309 Mean :0.561368 d :68150

## 25363 : 3 3rd Qu.:0.00000 3rd Qu.:1.000000 h :26748

## 25580 : 3 Max. :4.00000 Max. :1.990000 j :18074

## (Other):413939 (Other):36546

## CarAge DriverAge Brand

## Min. : 0.000 Min. :18.00 Fiat : 16757

## 1st Qu.: 3.000 1st Qu.:34.00 Japanese (except Nissan) or Korean: 79228

## Median : 7.000 Median :44.00 Mercedes, Chrysler or BMW : 19314

## Mean : 7.531 Mean :45.32 Opel, General Motors or Ford : 37477

## 3rd Qu.: 12.000 3rd Qu.:54.00 other : 9886

## Max. :100.000 Max. :99.00 Renault, Nissan or Citroen :218591

## Volkswagen, Audi, Skoda or Seat : 32707

## Gas Region Density

## Diesel :206350 Centre :160814 Min. : 2

## Regular:207610 Ile-de-France : 69989 1st Qu.: 67

## Bretagne : 42200 Median : 287

## Pays-de-la-Loire : 38829 Mean : 1987

## Aquitaine : 31399 3rd Qu.: 1410

## Nord-Pas-de-Calais: 27357 Max. :27000

## (Other) : 43372

## ClaimAmount

## Min. : 0.0

## 1st Qu.: 0.0

## Median : 0.0

## Mean : 83.3

## 3rd Qu.: 0.0

## Max. :2036833.0

##

nrow(df)

## [1] 413960

# Also delete large claims

# lc.idx = (df$ClaimAmount>sev.cutoff)

# lc.policy = as.integer(df$PolicyID[lc.idx])

# Delete invalid data

# df = df[!(df$PolicyID %in% union(del.policy,lc.policy)),]

df = df[!((df$CarAge > carage.cutoff) | (df$DriverAge > 98) |

(df$Exposure > exposure.cutoff) | (df$ClaimAmount > sev.cutoff)),]

# Check the merge is correct

summary(df)

## PolicyID ClaimNb Exposure Power

## 18652 : 4 Min. :0.00000 Min. :0.002732 f :95688

## 226856 : 4 1st Qu.:0.00000 1st Qu.:0.200000 g :91057

## 311457 : 4 Median :0.00000 Median :0.530000 e :77016

## 15608 : 3 Mean :0.04307 Mean :0.560563 d :67942

## 25363 : 3 3rd Qu.:0.00000 3rd Qu.:1.000000 h :26665

## 25580 : 3 Max. :4.00000 Max. :1.000000 j :18029

## (Other):412588 (Other):36212

## CarAge DriverAge Brand

## Min. : 0.000 Min. :18.0 Fiat : 16716

## 1st Qu.: 3.000 1st Qu.:34.0 Japanese (except Nissan) or Korean: 79199

## Median : 7.000 Median :44.0 Mercedes, Chrysler or BMW : 19231

## Mean : 7.464 Mean :45.3 Opel, General Motors or Ford : 37398

## 3rd Qu.:12.000 3rd Qu.:54.0 other : 9815

## Max. :30.000 Max. :98.0 Renault, Nissan or Citroen :217709

## Volkswagen, Audi, Skoda or Seat : 32541

## Gas Region Density

## Diesel :205918 Centre :160208 Min. : 2

## Regular:206691 Ile-de-France : 69825 1st Qu.: 67

## Bretagne : 42094 Median : 287

## Pays-de-la-Loire : 38710 Mean : 1987

## Aquitaine : 31310 3rd Qu.: 1410

## Nord-Pas-de-Calais: 27212 Max. :27000

## (Other) : 43250

## ClaimAmount

## Min. : 0.00

## 1st Qu.: 0.00

## Median : 0.00

## Mean : 65.38

## 3rd Qu.: 0.00

## Max. :96906.00

##

nrow(df)

## [1] 412609

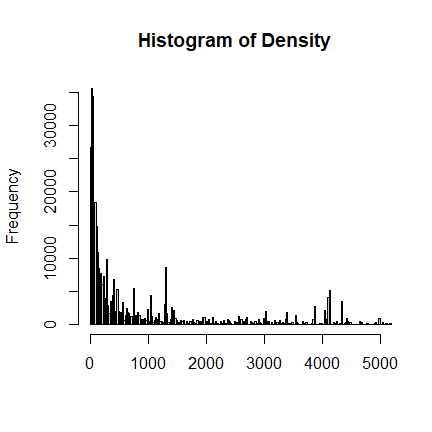

The summary and marginal histogram of ClaimAmount is given as follows.

summary(df$ClaimAmount)

## Min. 1st Qu. Median Mean 3rd Qu. Max.

## 0.00 0.00 0.00 65.38 0.00 96906.00

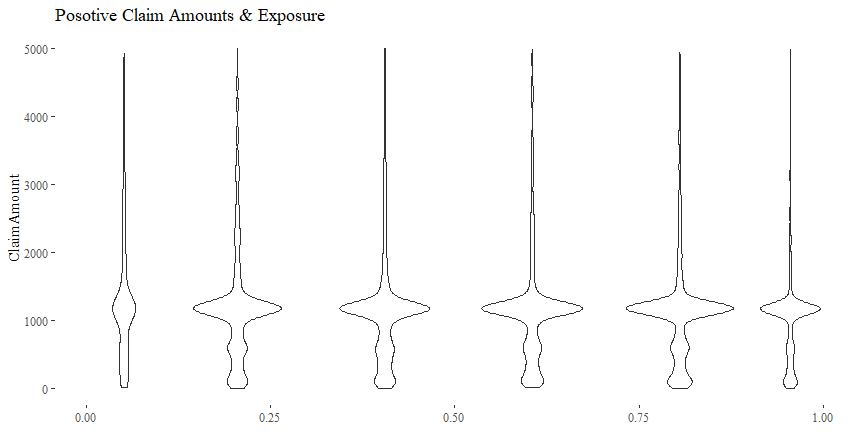

Claim Amount & Exposure

There is not really a discernible pattern of ClaimAmount plotted

against Exposure. Other than some outliers, the distributions of

ClaimAmount given different values Exposure seem quite similar.

cor(df$Exposure, df$ClaimAmount)

## [1] 0.01651165

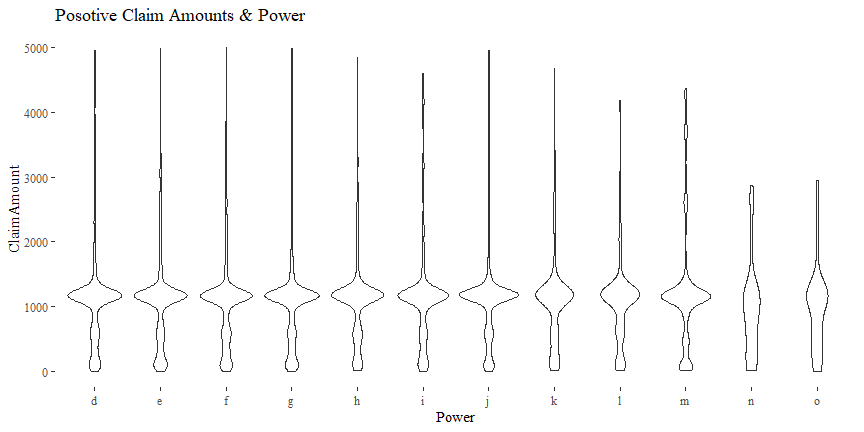

Claim Amount & Power

There might be some relationship between ClaimAmount and Power.

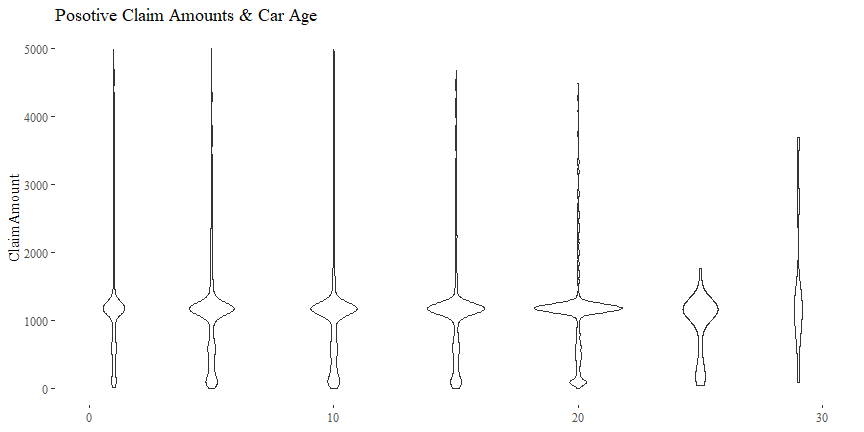

Claim Amount & Car Age

There might be some relationship between ClaimAmount and CarAge.

cor(df$CarAge, df$ClaimAmount)

## [1] -0.002292825

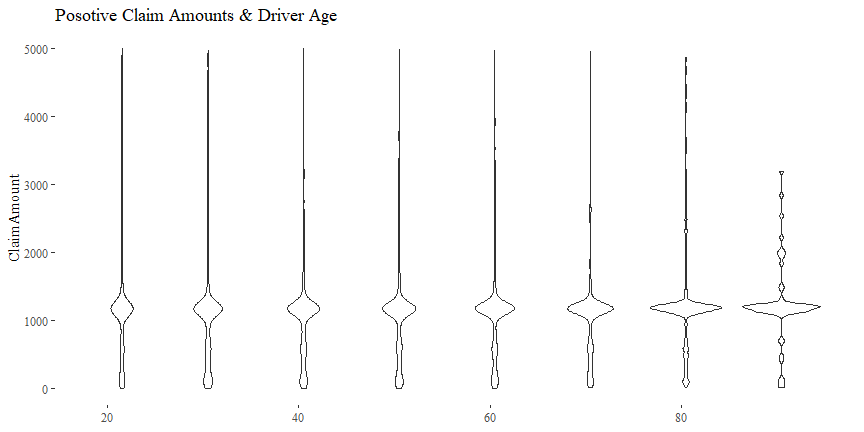

Claim Amount & Driver Age

There might be some relationship between ClaimAmount and DriverAge.

cor(df$DriverAge, df$ClaimAmount)

## [1] -0.002324578

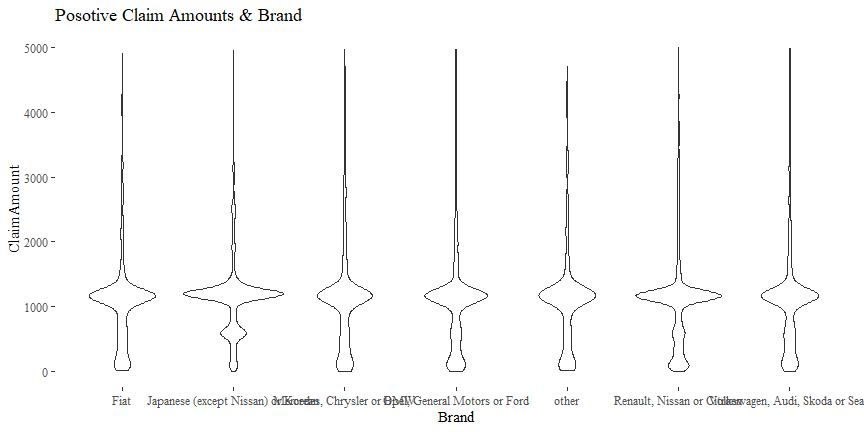

Claim Amount & Brand

There might be some relationship between ClaimAmount and Brand.

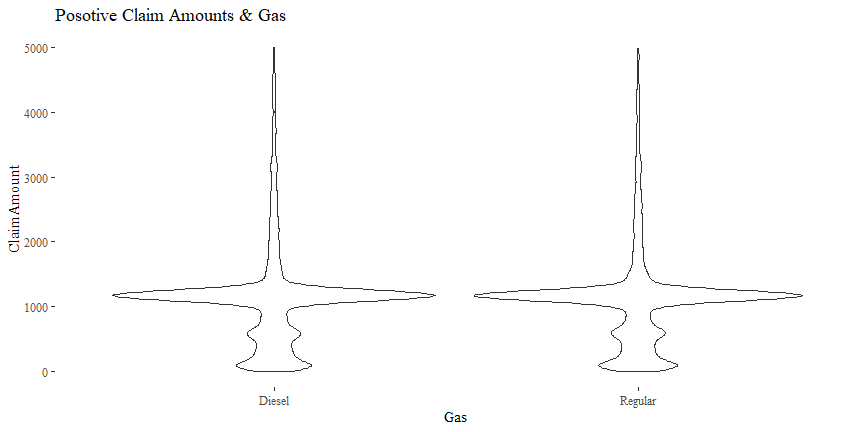

Claim Amount & Gas

The relationship between ClaimAmount and Gas is not quite clear.

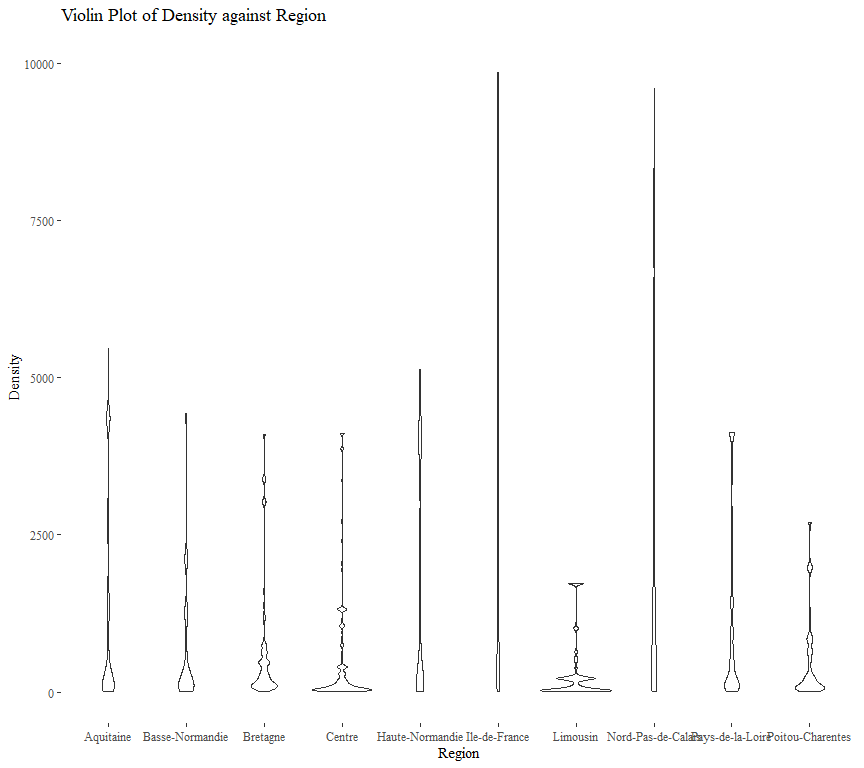

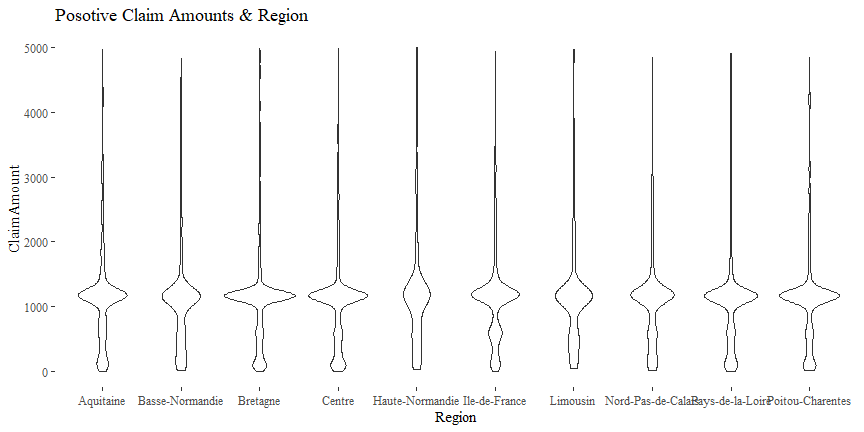

Claim Amount & Region

There might be some relationship between ClaimAmount and Region.

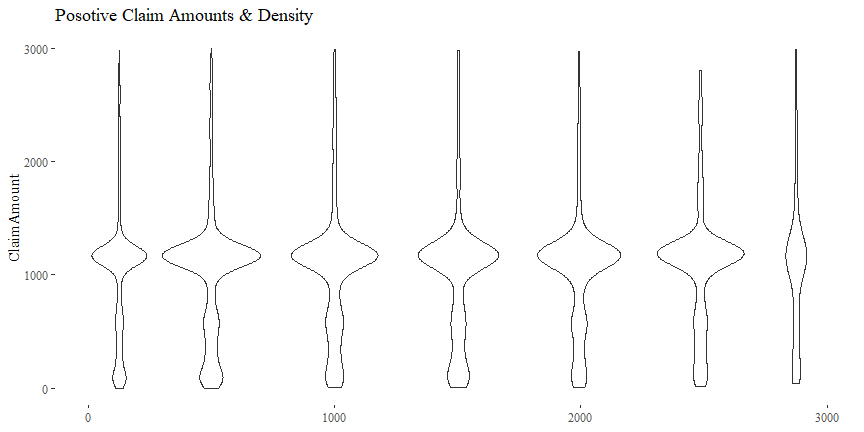

Claim Amount & Density

There might be some relationship between ClaimAmount and Density.

cor(df$Density, df$ClaimAmount)

## [1] -0.0009410736

Saving Data

We will save the cleaned datasets for further analysis.

save(df, file = "freMTPLClean.Rda")